There are two takes on that: 1. Have we already experienced inflation in local commodities (rent, food, insurance, property tax, labor) and the media/government is ignoring it or concealing it by continually measuring inflation based on foreign goods? Sure it is great that Chinese made dress shirts now cost $20, but my homeowner's insurance is up 20% from five years ago - and don't even get me started on what the plumber bid to repair the leak! We are continually told that we are NOT experiencing inflation, yet things cost more.

2. The wages of the working population need to increase to facilitate inflation. After all, inflation is the increase in the price level of goods and services in an economy over time. There must be excess currency in the economy to facilitate the price level increases. Wages have not increased enough for the middle and lower class. Wages have increased for the upper class, but this is not enough to actualize inflation.

In April 2015, we are seeing big business increasing wages across the board. This has been the one "finger in the dam" the Fed has been unable to plug over the last five years (or they were in cahoots with these big businesses to hold off on wage increases). Now that wages are starting to increase, the economy will speed up, inflation will be "recognized" and interest rates will rise.

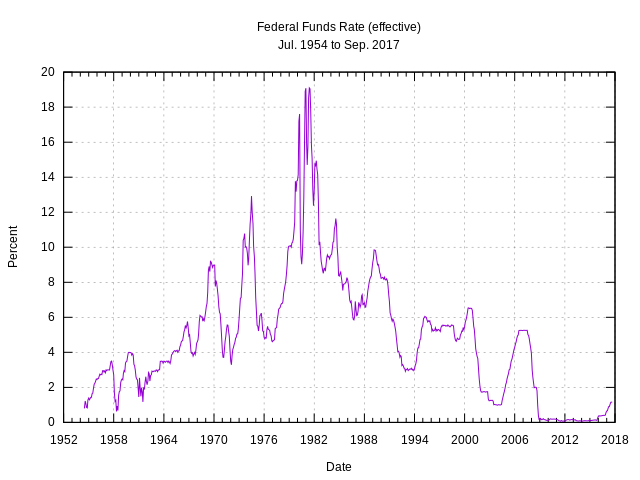

Frankly, inflation has been here and gone and there is not an asset bubble in housing. We are now paying at least 20% more for domestic goods and services that we were five years ago. The media/government has had foreign imports and a strong dollar to keep "virtual inflation" low or deflationary. Housing prices are up, but it is a matter of supply and demand. Only preferred markets are seeing the price increases. Now the Fed must re-set its "recession" tool and return the Fed Funds rate to sustainable levels. Where would we be if there was another near financial collapse and the Fed had no tools to utilize? We sure know they can stop inflation dead in its tracks at this point with a solid rate hike. That is how the rate hike will play out and be publicized.

As always, there are bargains to be had in any market and real estate is always a solid investment. We are available to work shop and discuss these ideas at www.FirstAmericanMortgage.net

Thank you!

No comments:

Post a Comment